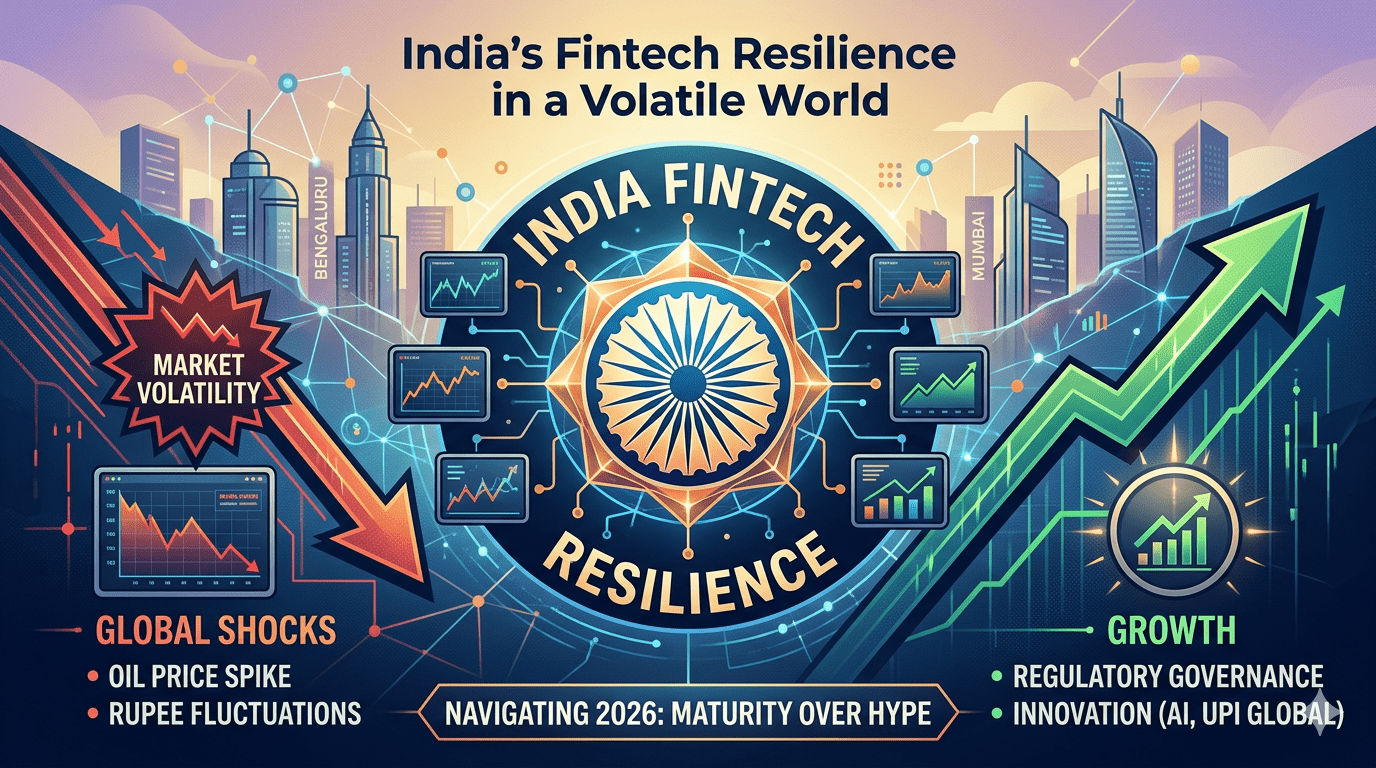

In March 2026, the “Golden Age” of Indian fintech is facing its most significant stress test yet. As geopolitical tensions in West Asia—specifically the Iran-Israel conflict—escalate, the ripple effects are being felt across Dalal Street and the digital corridors of Bengaluru. However, beneath the surface of market volatility lies a story of a sector that has matured from a growth-obsessed teenager into a governance-led institution. This article explores how India’s fintech landscape is navigating the “War-Time” economy of 2026.

1. The Market Shock: Crude, Currencies, and Corrections

The most immediate impact of the 2026 conflict has been the “Risk-Off” sentiment dominating Indian markets.

- The Crude Trigger: As of March 12, 2026, Brent crude has surged, briefly spiking toward $100 per barrel due to potential disruptions in the Strait of Hormuz.

- Equity Bloodbath: Benchmark indices like the Nifty 50 and Sensex witnessed sharp intraday drops in early March, with the Nifty falling below the 24,000 mark as foreign institutional investors (FIIs) pulled capital.

- Rupee Under Pressure: The Indian Rupee hit a record low of 91.08 against the USD on March 2, driven by higher import costs for oil and electronics.

Fintech Impact: For wealthtech and brokerage platforms like Upstox and Groww, this volatility has triggered a surge in trading volumes as retail investors pivot toward short-term debt funds and safe-haven assets like gold.

2. The “Reality Check”: Consolidation and Quality

The “Funding Winter” of 2023–2025 has effectively weeded out unsustainable models. By early 2026, the mantra has shifted from “Growth at All Costs” to “Governance as Competitive Edge”.

- The Great Shakeout: Over 700 startups shuttered between 2023 and 2025, leaving behind “battle-tested” firms with proven unit economics.

- IPO Readiness: Mature players in lending and insurance are now seeking listings, provided they meet the SEBI profitability track record of ₹15 crores average operating profit over three years.

- Focus on Lending: Digital lending now accounts for nearly 60% of fintech funding, as investors favor the predictable returns of credit over the high-burn customer acquisition models of pure-play payments.

3. Regulatory Guardrails: The 2026 Reset

The RBI has moved from being a passive observer to an active architect of the ecosystem.

- New Digital Banking Directions: Effective January 1, 2026, these rules mandate stricter customer consent and enhanced cybersecurity for all banking-fintech partnerships.

- Digital Lending Crackdown: To curb unethical recovery and hidden charges, the RBI now requires all loans to flow directly from Bank → Customer → Bank, effectively ending the era of unregulated “mini-banks”.

- KYC Modernization: Updated KYC compliance rules (March 1, 2026) have simplified digital onboarding while making periodic updates mandatory to combat fraud.

4. Emerging Growth Engines: AI and Global UPI

Despite the external chaos, internal innovation is accelerating through “Agentic AI” and the globalization of the India Stack.

- Agentic Payments: Companies like Razorpay and Juspay are moving toward AI-led commerce, where autonomous agents handle authorization, fraud monitoring, and compliance in real-time.

- UPI Without Borders: India is aggressively exporting UPI to Southeast Asia and the Middle East, reducing reliance on Western-dominated payment rails and enhancing “strategic autonomy”.

- Embedded Finance: Financial services are becoming an “invisible layer” within e-commerce (ONDC) and logistics platforms, moving away from being siloed apps.

Conclusion: The New Normal

India’s fintech sector in 2026 is no longer a collection of “wild startups” but a pillar of national infrastructure. While the war in West Asia creates short-term turbulence, the industry’s focus on trust, transparency, and domestic resilience suggests that India is no longer just catching up—it is setting the global benchmark. Would you like a deeper analysis of the specific RBI regulations taking effect later this year, such as the UPI Security Framework coming in June?